Stephane Tajick

Last updated: January 8, 2018

Congress gave its final approval to the House and Senate conference committee agreement on tax reform legislation (HR 1), providing the largest changes in U.S. tax policy in the last 30 years. The reform will affect corporate tax, personal income tax and move the “worldwide taxation” to a 100 percent dividend exemption ‘territorial’ system.

For those not familiar with U.S. taxation, taxes are levied by the federal government, the states, and in some cases, the municipalities. The tax reform only affects federal tax rates.

The effective date of the rate reduction would be January 1, 2018. At this time, President Trump hasn’t signed the legislation into law. The actual signing could take place in January 2018 because of an increases in federal budget deficits that could trigger automatic cuts to various federal spending programs due to the ‘pay-as-you-go’ (‘PAYGO’) statute.

The Joint Committee on Taxation estimates an increase in economic output (as measured by Gross Domestic Product) by about 0.8 percent on average over 10 years. It would offset the $1.414 trillion estimated revenue loss of the Finance Committee bill to just over $1 trillion over 10 years.

Highlight of the Changes for Businesses

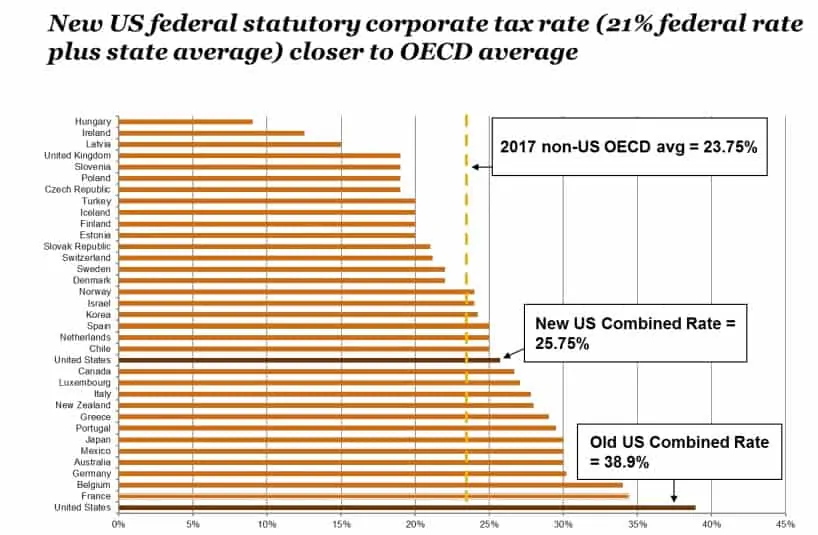

The U.S. boasts the highest corporate tax rate in the world; in New York City, corporate tax can hit a rate of 50 percent when state and city rates are added. The changes will permanently reduce the federal rate from 39.6 percent to 21 percent. Certain business deductions will be limited with the new reforms and the Corporate AMT will be repealed by 2018. The changes will also create a 20 percent deduction for the non-wage portion of Passthrough entities income. Dividends earned abroad will be tax-exempted, but additional provisions will be put in place to safeguard the U.S. tax base from erosion.

Source: PWC

Highlights of the Changes for Individuals

The reforms will also affect the personal income tax rate at the federal level, by lowering the top rate from 39.6 percent to 37 percent and revising the brackets; certain deductions will be repealed. The Conference Agreement would maintain the estate, gift, and generation-skipping transfer taxes (currently at 40 percent). The agreement would double the exemption from $5,600,000 to $11,200,000 per person. Theses changes will not be permanent and will end in 2025.

Source: PWC

The Economic Impact

HR1 has been labelled as a protectionist bill as it offers both stick and carrots to businesses conducting business offshore, also laying the groundwork to welcome the Saudi Aramco IPO. The reduction in corporate tax rate was something to be expected, not only because President Trump made it a campaign promise, but because these rates were so high that the nation was deemed the “champion of capitalism.” Nevertheless, expectations would have been that the reduction would be gradual so that the U.S. economy would absorb it in a fashion that it could adapt and provide benefits to all. Such drastic changes usually cause a shock to the economy and are usually preferable when that economy is in a recession or performing below potential. This is not the case for the U.S., which currently has been showing sign of performing to its potential and is currently healthier than other developed economies. As accurately estimated by many, the gain will be felt mainly on Wall Street and the higher reaches of the business community. By making the changes sudden rather than gradual, the trickle-down effect will be lessened. A profitable company is unlikely to suddenly hire more staff if it doesn’t make sense from an operating point of view. The bill also raises the questions over the inequality between states. Well-performing states like New York or California are the main winners of the reform and the gap between rich and poor states is expected to widen. Here is what can be expected to happen in 2018:

What It Means for the EB-5

The tax reform is unlikely to have any direct impact on the EB-5. It might have caused a slowdown to the EB-5 reform for a while as it was taking center stage in 2017. For the EB-5 not to lose any “panache” next to the economic development package offered by the tax reforms, it will need to highlight its contribution to the targeted areas with high unemployment, places that are unlikely to receive most of the gains from the HR1 reforms.

As can be expected, the industry will reduce its tax liability. For the EB-5 immigrants, those changes mean lower income tax, no tax on corporate foreign dividends, and the increase of the deduction on estate and gift taxes.

The negative impact on EB-5 might be vague. With so much money flowing into the market from the general tax cut, there might be more competition to supply capital. Regional centers might have to turn to riskier projects. The tax cut will lead to more money floating around and lower access to capital, which might come in competition with the EB-5. This can be curbed if the Federal Reserve increases its rate. For the EB-5 investor settling in New York, Los Angeles, and other in-demand cities, he can expect rising property prices or, for those arriving shortly, a nice increase on the value of their property in the not-so-distant future.

| INTERNATIONAL BUSINESS TAX REFORM PROPOSALS | |

| Current law | Conference Agreement |

| Corporate tax rates 35% rate | 21% rate for tax years beginning after 12/31/2017. A blended rate applies for fiscal year taxpayers. |

| Corporate AMT 20% rate | Corporate AMT repealed after 2017. Prior year AMT credits refundable from 2018 to 2021. |

| Business interest expense Deductible as incurred | One test would apply: Limited to the sum of business interest income plus 30% of the adjusted taxable income of the taxpayer for the taxable year. Adjusted taxable income is defined similar to EBITDA for taxable years beginning after 12/31/2017 and before 1/1/2022, and is defined similar to EBIT for taxable years beginning after 12/31/2021. Would not apply to certain regulated public utilities and certain electric cooperatives, floor plan financing interest, and at the taxpayer’s election certain real property trades or businesses. Limitation applies to both related party and unrelated party debt. Disallowed interest is allowed to be carried forward indefinitely |

| Pass-through entities Income is passed through to the owners to be taxed at the individual rates. | Creates a 20% deduction for non-wage portion of passthrough income. Deduction is limited to the greater of (a) 50% of the W-2 wages paid with respect to the qualified trade or business, or (b) the sum of 25% of the W-2 wages with respect to the qualified trade or business plus 2.5% of the unadjusted basis, immediately after acquisition, of all qualified property for taxpayers with income over $315,000 (married) or $157,500 (individuals). The 50% limit is phased in over the next $100,000 (married) of taxable income ($50,000 for individuals). The conference agreement broadens eligibility requirements to include income from trusts and estates. The deduction does not apply to specified services business income, except when income of taxpayers married filing jointly does not exceed $315,000 ($157,500 for individuals). The benefit of the deduction is phased out over the same limits as above. Sunsets after 2025. |

| Net operating losses Carryback up to 2 years and carryforward up to 20 years | Limit to 90% of income, indefinite carryforward; no carryback. Limits to 80% of taxable income (determined without regard to the deduction) for losses arising in tax years beginning after 12/31/2017 |

| Revision of treatment of contributions to capital The gross income of a corporation generally does not include contributions to its capital. A debtor corporation that acquires its own debt from a shareholder as a contribution to capital generally will not recognize cancellation of debt income except to the extent the shareholder’s basis in such debt is less than the adjusted issue price. | Preserves the current provision under which a corporation’s gross income generally does not include contributions to capital, but provides that the term “contributions to capital” does not include (1) any contribution in aid of construction or any other contribution as a customer or potential customer, and (2) any contribution by any governmental entity or civic group (other than a contribution made by a shareholder as such). Section 118, as modified, continues to apply only to corporations. |

| Entertainment deduction Employers may deduct 50% of business-related entertainment costs. | Repeals deduction |

| International tax regime ‘Worldwide’ system foreign tax credits to mitigate double taxation | ‘Territorial’ system 100% foreign dividend exemption |

| Repatriation ‘toll tax’ Currently no provision. Previously untaxed foreign earnings: • 35% corporate rate when repatriated with foreign tax credit | Previously untaxed foreign earnings: • 15.5% cash and cash equivalents • 8% non-cash assets • Payable over 8 years in increasing installments • Proportional reduction in foreign tax credits attributable to previously untaxed foreign earnings |

| Anti-base erosion regime (Subpart F) Subpart F anti-deferral regime includes CFC’s insurance income, foreign base company income, etc., with foreign tax credit | Follows Senate bill with certain modifications. Specified return is equal to 10% of shareholder’s aggregate pro rata share of QBAI and is reduced by interest expense taken into account in determining net CFC tested income. GILTI after the 50% deduction is effectively taxed at 10.5% (13.125% after 2025) before consideration of foreign taxes. |

| Incentive for US production for sale to foreign customers Not provided | A 37.5% deduction is allowed for foreign-derived intangible income produced in the US. The deduction is reduced to 21.875% for tax years starting after 12/31/2025. |

| Foreign tax credit A taxpayer can generally take a credit or deduction for foreign taxes paid or accrued. US shareholder may be deemed to pay foreign income taxes paid by a foreign corporation when the US shareholder receives a dividend from a foreign corporation or includes earnings of a foreign corporation in gross income. | Repeals deemed paid tax credit for dividends received from a foreign corporation. Retains deemed paid tax credit for subpart F inclusions. Proposal eliminates need for computing and tracking cumulative tax pools. No foreign tax credit or deduction permitted for any taxes paid or accrued with respect to any dividend subject to the new deduction for foreign dividends. |

| Transfers of property from US to foreign corporation In general, an exchange in which a US person transfers property to a foreign corporation is not eligible for non recognition treatment. Under the active trade or business exception, certain property transferred to a foreign corporation for use in the active conduct of a trade or business outside of the United States is eligible for non recognition. | Repeals the active trade or business exception. |

| INDIVIDUAL TAX REFORM PROPOSALS | |

| Current law | Conference Agreement |

| Individual rates Seven rate brackets (10%, 15%, 25%, 28%, 33%, 35%, and 39.6%) | Seven rate brackets (10%, 12%, 22%, 24%, 32%, 35%, and 37%). Sunsets after 2025. |

| AMT imposed when minimum tax exceeds regular income tax. | Increases individual AMT exemption amounts (same as Senate bill) and phase-out thresholds (higher than Senate bill). Sunsets after 2025. |

| Individual – standard deduction $6,500 for single filers/ $13,000 joint filers (2018) | $12,000 for single filers/ $24,000 joint returns (adjusted for inflation based on chained CPI). Increased deduction sunsets after 2025. Chained CPI does not expire after 2025. |

| Personal exemption $4,150 for each person, spouse, and dependents (2018) | Repeals deduction for personal exemptions. Sunsets after 2025. |

| Mortgage interest deduction Mortgage interest deduction limited to acquisition debt of $1 million and home equity debt of $100k on a principal and second home. | Retains current law limitation for existing acquisition debt; acquisition debt limited to $750,000 for newly purchased homes, available for a first or second home. Repeals deduction for non-acquisition HELOCs. Sunsets after 2025. |

| Estate Tax Maximum 40% rate for taxable estates exceeding $5.6 million (2018 indexed amount) | Doubles exemption amounts. Sunsets after 2025. |

Source: PWC FOR FURTHER READING

“Our purpose is to provide information, so feel free to contact us if you need more. If you need professional help, let us know, and we will direct you toward a trusted expert in your area.”

Need help?

Navigating through golden visa & citizenship by investment programs can be complex and overwhelming, regardless of the country or program you’re interested in. If you’re struggling to find clear, accurate information, you’re not alone. Our team is here to offer you clarity and reliable advice across a wide range of immigration programs.

By scheduling a consultation, you’ll receive personalized guidance tailored to your unique situation. We’re dedicated to helping you understand the details of various immigration programs, making them more straightforward so you can proceed with confidence.

During our call, we will:

Here is what to expect from a call with our advisory team:

We’ll answer your questions about the program and the application process, providing you with the clarity you need.

We’ll break down each stage of the immigration process, ensuring you know exactly what to expect.

We’ll help you determine if the chosen program is the right fit for you or suggest alternatives that may better align with your goals.

Gain access to our network of recommended local lawyers, as well as providers of eligible investment options.

Read more articles about citizenship and residency below

Request a free consultation

[contact-form-7 id="8" title="request"]